It’s said that bigger isn’t always better, and this is especially true when it comes to private equity investing. In fact, when we look at the growth of private-equity-owned companies and private market assets under management (AUM) during the past decade, it would be easy for the layman to survey that 170 percent growth and salivate at the thought of staking their share.

However, this type of burgeoning growth can have a curious side effect – it can assure a landscape rife with swollen funds producing mediocre returns, managed by a team that is satisfied to dine on the 2 percent management fee and is swerving around risks like potholes.

So how can one outperform in a market that continues to level off amid heavy competition? We believe that a tremendous upside exists with emerging managers – those that have decided to break off from the pack and invest drive and vision – and often a personal stake of capital – to raise their first few funds.

We at Oxford find that emerging managers, with their determination and built-in incentive to succeed, represent a great alternative to traditional private equity. We find that larger private equity funds tend to take a substantial commitment of resources, both personnel and organizational infrastructure, and offer an upside that is often occluded by illiquidity, deal dynamics and opaque sharing of information.

Emerging managers, on the other hand, are incentivized to share details and, due to the modest amount of AUM, are dependent upon a share of the profits more than a management fee to earn a living. Though it may seem counterproductive to use a young upstart to manage your assets, there are a decent amount of safety gates through which emerging managers must pass in order to make the cut. These include:

I. Track record: We evaluate the track record at prior institutions – what types of investments they worked on, the performance of their investment mix and so on.

II. Role: Through conversations with other managers, the CEO, CFO, board chairman and others, we define how they were involved in the results they are touting. Were they simply executional in nature or did they take the lead in defining the investment choices?

III. Intermediaries: We check other references to corroborate their role in producing the results they are taking credit for.

IV. Hunger: In talking to the manager directly, we are as interested in their passion for the pursuit of excellence as we are in the actual numbers. Are they hungry for success?

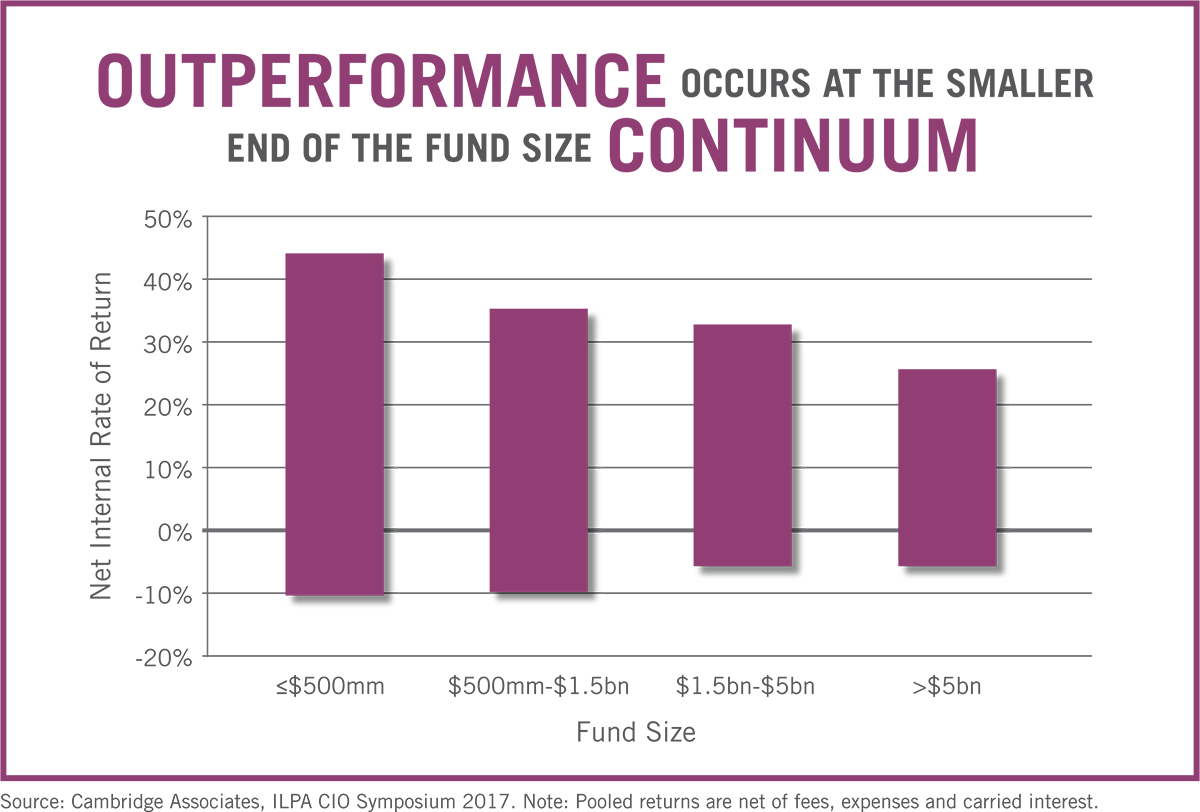

A study published by private markets consulting firm, Cambridge Associates, affirms the value of emerging managers. It found that, although the range of outcomes for smaller funds is greater, the potential magnitude of increased gains significantly outweighs the magnitude of the potential increase in losses.

We at Oxford will continue to pursue a diversified portfolio of emerging managers. Through this strategy, our hope is that Oxford clients can capture outperformance in an increasingly competitive environment.